Dollar Wrecking Ball 2.0

Will the DOLLAR IMPLODE Global Markets?

The dollar is climbing again. The DXY pushed up to a one-year high. The yen broke through the one sixty taboo line again. The market started pricing the possibility that the Fed may even hike from here. None of that is good news. A strong dollar sounds good for the United States and bad for the rest of the world, but the mechanics of what is actually happening are far more brutal than the headline version.

The market read the latest dot plot and rewrote the script in a matter of days. The Fed held rates flat, but the distribution of the dots made it clear that cuts are off the table. A hike is back on the menu of scenarios any leveraged portfolio has to consider. When that view sets in, capital runs to the safe port. The safe port is the dollar. The reaction shows up immediately in the rest of the currency board. Japan is signaling concern about the yen again, with intervention back in the air. The Real, which had been running as the best-performing currency in the world, is starting to give the move back.

Currency strength is an INVERTED game, and that is the key almost no one catches. A weaker dollar does NOT mean a dollar that is dying. It means exactly the opposite. When the dollar weakens, the system is dolarizing the rest of the world, exporting liquidity through credit and leverage. The only way to keep that machine alive is by creating more dollars outside the United States. That has a name. It is called the eurodollar system, and it is where most of the dollars on the planet actually live. When the dollar reverses up, the screw turns back. Every country that took on cheap dollar debt has to pay expensive dollar back. Every balance sheet that was long dollar leverage gets margin-called. That is the plumbing of the system running in the opposite direction of what the headline says.

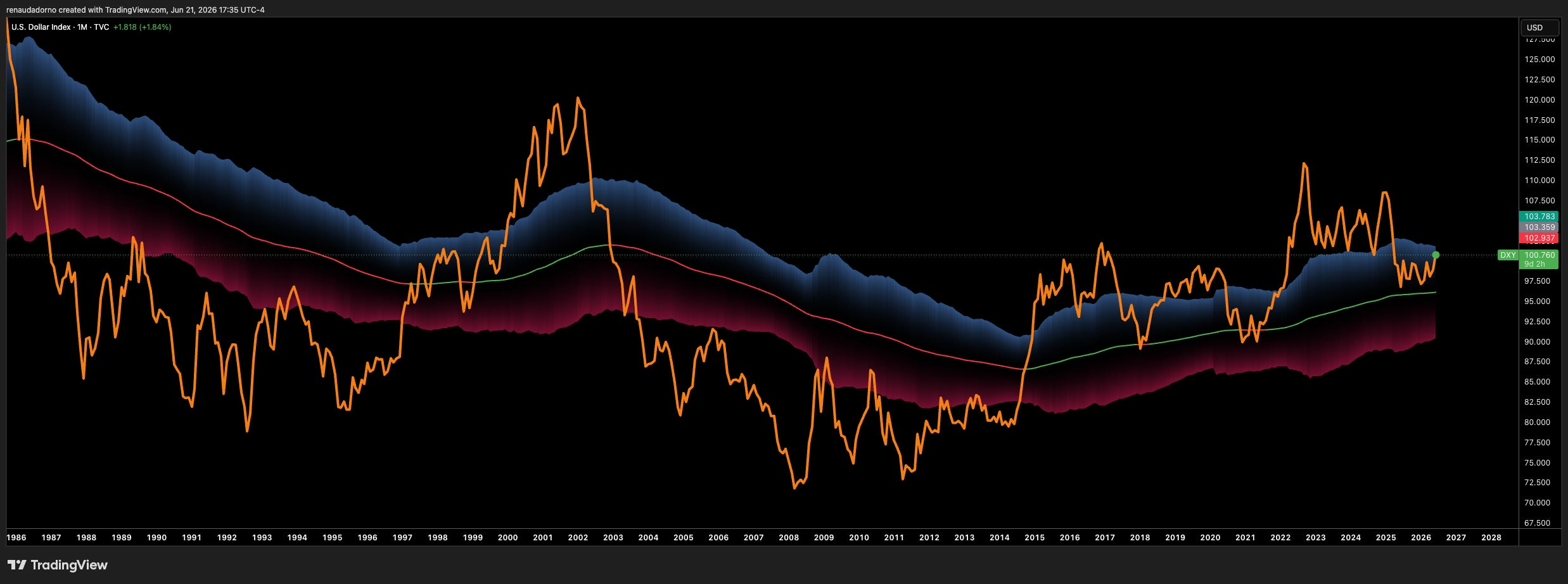

The DXY has been structurally tightening since 2008

When the DXY chart gets pulled out to the long run, the story turns transparent. In March of two thousand and eight, in the exact moment the world looked like it was ending, the index was at SEVENTY-TWO. The global monetary system still ran on the old logic: bank trust, free derivative expansion, dollars flowing into Asia, Europe, and Latin America. After 2008 the regime changed for good. The DXY never came back near those levels. Except for a brief touch of seventy-three in 2011, every move since then has been up. The dollar stopped being exported with the same generosity, and that shows up on the chart as a staircase climbing.

That tightening is not narrative, it is mechanical. After 2008 credit stopped working on trust and started requiring collateral. And the only collateral that survived the test was the US T-bill. Derivatives, corporate bonds, debentures, every instrument that used to clear without questions became suspect. The result is a structural suppression of global liquidity. Dollars in circulation become more valuable. Lenders think twice. Borrowers pay more. That is the system we have been living inside for more than fifteen years, and it keeps reinforcing itself.

The dollar-dying narrative never actually met the chart

The entire first half of two thousand and twenty-five was hijacked by the thesis that the dollar was being destroyed. Global dedollarization. Nobody wants dollars anymore. Paper is going to zero. The DXY drop down to ninety-five in January was treated as the beginning of the end. The whole debasement trade ran on top of that. Gold ripped. Emerging market equities ripped. The Ibovespa climbed. The Real had its strongest relative performance in years. The move was real, but the reading behind it was wrong. The DXY never even approached the long-term two-hundred-month line. It touched support around one hundred point seven, held, and is now reversing up. The post-2008 monetary system did not even let the experiment through the door.

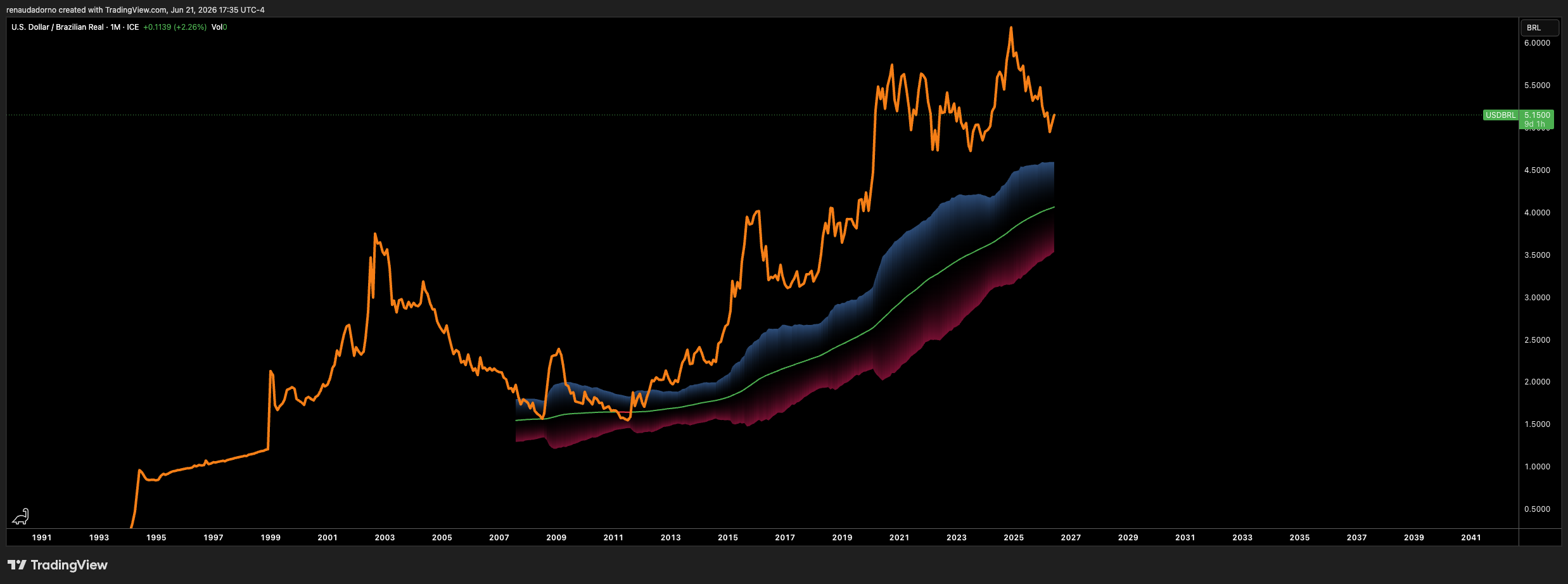

The Brazilian Real is leveraged to dollar flow, not to its own strength

The Real is the newest currency on the global chessboard. When the chart is pulled back to its creation in nineteen ninety-four, the reading is unambiguous: the Real does one thing over time, which is lose value to the dollar. The stretches in which it appears to beat that gravity are precisely the windows when the global system is exporting dollar liquidity. Brazil has an economy. Brazil has reserves. Brazil has every condition to participate in the easing phase of the cycle. But that strength is conditional on the flow continuing. The minute the screw turns back, the Real returns to what it has always been. That dependency on flow is the biggest structural risk in the Brazilian market right now.

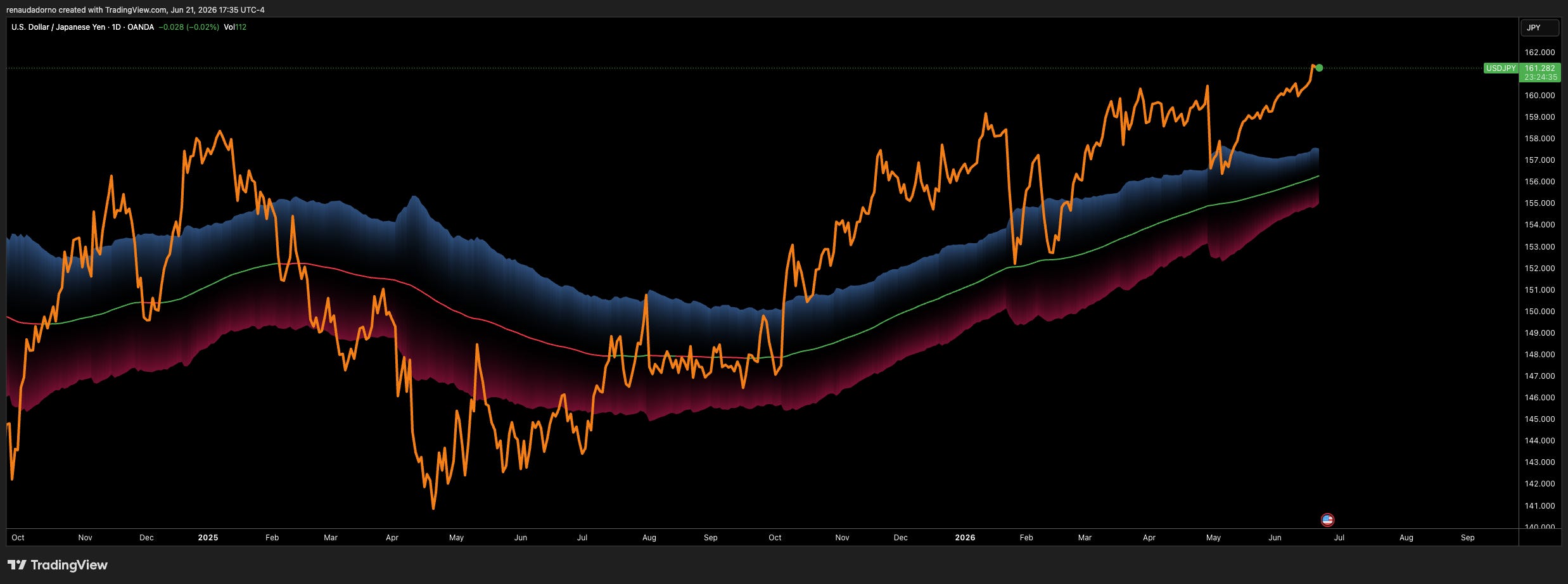

The yen above 160 is the cleanest stress gauge in the system

Anyone who follows Japan knows what one sixty carries as a number. The yen used to be the easy currency to math, calculated near one hundred to the dollar. It now operates in a different universe. The Bank of Japan has shown willingness to intervene every time that threshold is broken, and the current candle is sitting right on top of it. Each push higher pressures the Japanese economy from the inside, feeds an inflationary wave through the monetary channel, and forces the government to either burn reserves or accept the devaluation. The yen is the cleanest thermometer of what is happening to the plumbing of the system, and it is sending a message.

The S&P 500 is still giving the temperature of leveraged capital

The S&P 500 keeps doing what the S&P 500 does best: it circulates global capital and returns the temperature of risk in real time. The whole Iran story is reflected in the candles. The negotiation happening in Switzerland between the delegations will show up in Monday's futures open. There is an optimistic reading, defended by serious analysts like Robin Brooks, that the dollar strength is transient because Kevin Warsh is not going to hike, the dot plot is not going to confirm, and risk assets resume the climb. That may well be right in the short run. But it ignores the structural force that has been quietly tightening since 2008 and is reasserting itself now. Volatility is guaranteed in the next few days. What needs to be on the radar is what comes after.

Dollar Wrecking Ball 2.0 is officially on the radar

The United States is the only country in the world with the ability to push the dollar down. When the dollar is going up, nobody has full control, because the eurodollar system lives outside the reach of US monetary policy. When the dollar needs to go down, Washington can move it. That is the central detail. Over the next few months, with the Fed on hold, the dot plot hawkish, the yen under pressure, and the Real giving back gains, every condition is in place for what could be a second version of the Dollar Wrecking Ball. The administration does not want that and will fight it. But the structural mechanics of the post-2008 system are still driving the car. And those mechanics do not ask permission from any administration.

The dollar returning to its one-year high while the yen, the Real, and the rest of the emerging world start to feel it is exactly the kind of configuration that has to be respected after living through 2008, 2015 and 2022. Every time the eurodollar screw turns in the direction of tightening, something somewhere breaks. Reading this as tactical noise will require explaining the long-run DXY chart. Reading it for what it is, a structural macro force coming back to the front, buys positioning time before consensus catches up.

Source:

https://www.cnbc.com/2026/06/18/dollar-holds-at-two-month-peak-as-fed-rate-hike-bets-mount-yen-slides.html